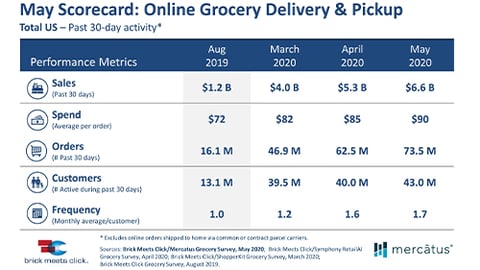

Dual-Channel Grocery Shopping Surges

According to the “2020 U.S. Online & In-Store Grocery Shopping Study” from the Retail Feedback Group (RFG), which offers a broad spectrum of research, consumer insight and consulting services, dual-channel shopping has become much more common amid the coronavirus pandemic, especially among younger consumers.

Overall, 50% of in-store supermarket shoppers in the past 30 days also ordered groceries online, the report found, adding that this tendency was even more common among Gen Z (66%) and Millennial (61%) consumers, and, to a lesser degree, Gen X (52%), trailed by Boomers (37%) and the Silent Generation (38%). Notably, Gen Z shoppers expressed the lowest overall satisfaction, on a five-point scale where five is highest, compared with the other demographics, for both their online (4.22) and in-store (4.02) experiences.

“Grocers and analysts have traditionally segmented ‘in-store shoppers’ from ‘online shoppers,’” noted Doug Madenberg, principal at Lake Success, New York-based RFG. “However, a key takeaway from our research is the extent to which individual shoppers are now buying groceries both in a store and online, and that this activity is strongest among the younger and growing generations. We now have food shoppers who are able, and increasingly willing, to utilize a blend of physical stores and digital storefronts to meet their families’ needs, and it will be paramount to satisfy these shoppers going forward.”

While 38% of shoppers used one online grocery provider, 62% used two or more providers in the past three months, according to RFG, which noted that this finding indicated that many shoppers tried various services to determine which could best meet their needs in such areas as product availability and pickup or delivery slots.

Thirty-four percent of online shoppers identified a supermarket as where they most recently shopped online for groceries during the pandemic, up from 22% last year. Walmart continued to see the highest overall percentage of shoppers, at 40%, a slight increase from 2019’s 37%, while Amazon declined considerably, sliding from 29% last year to 14% this year. Instacart-fulfilled orders increased to 36%, up from 27% in 2019. Despite the pandemic surge, however, supermarket shoppers make up the largest percentage saying that they plan to shop less for grocery items online in the coming year (20%), compared with Walmart (16%) and Amazon (13%) customers.

Overall satisfaction among online shoppers measured 4.38 on a five-point scale, down from 4.48 last year. All channels showed lower overall satisfaction versus the previous year, but marks were still relatively high with Amazon in the lead (4.47), paced by Walmart (4.38) and supermarkets (4.33). The Instacart-fulfilled subset saw overall satisfaction of 4.35, a decline from 2019’s 4.48.

“Considering the sudden, sizeable pressure on online grocery shopping during the pandemic, it is noteworthy overall satisfaction registered as high as it did,” observed RFG Principal Brian Numainville. “Although supermarkets surged in online shopping use, and many customers may stick, the results show some supermarket shoppers don’t expect to continue online shopping. With that in mind, it will be important that supermarkets and online service providers maximize their investment by continually strengthening their offerings in order to retain existing customers, while attracting new ones, along with preparing for any future situations.”

In-store supermarket shoppers rated cleanliness of the store, on a five-point scale, at 4.41 and quality/freshness of the food and groceries at 4.37, as the most important core experience factors. Associate friendliness received the highest service rating, at 4.30, followed by checkout speed/efficiency (4.25), associate helpfulness/knowledge (4.16) and associate availability (lowest service rating, at 4.12). Meanwhile, item variety and selection dropped to 4.00 from 4.38 last year, and value for money, once more at the bottom of the list, fell further yet to 3.93, from 4.17 last year. Overall satisfaction was at 4.08, down from 4.31 in 2019.

Stock levels were a major challenge for in-store and online shoppers alike. About half of in-store supermarket shoppers (51%) said that the store they shopped didn’t have everything they wanted to buy. Results were similar for online food shoppers, with 49% noting their inability to purchase everything they wanted because of out-of-stocks, only 17% able to find an acceptable substitution for all out-of-stock products, and a considerable 45% didn’t end up getting all of the items they ordered. Since positive in-stock conditions result in higher satisfaction, these out-of-stock conditions caused not only lost sales, but also lower overall satisfaction.

Whether they purchased items online or in stores, a little more than half of the shoppers (54%) expressed a high amount of confidence that the food they bought during the pandemic was safe to eat, while 44% noted that they were only somewhat confident. For those shopping in a supermarket, only 33% were confident it was safe to do so.

Fifty-five percent of shoppers, either in store or online, said that they were shopping less often during the pandemic, with 51% noting that they spent more per trip. As a result, shoppers also said that they now stockpile products for longer amounts of time. For example, more shoppers keep two to four weeks of meat/seafood on hand at the present time (55%) whereas before, the majority kept just one week (52%). Regarding produce, while the majority of consumers still keep only one week of produce (57%) compared with before the pandemic (73%), some shoppers now keep two to four weeks (39%, versus 25% pre-pandemic).

RFG’s study was based on a nationally representative sample of 2,000 respondents who shopped in store and/or online for food and groceries in the past 30 days.